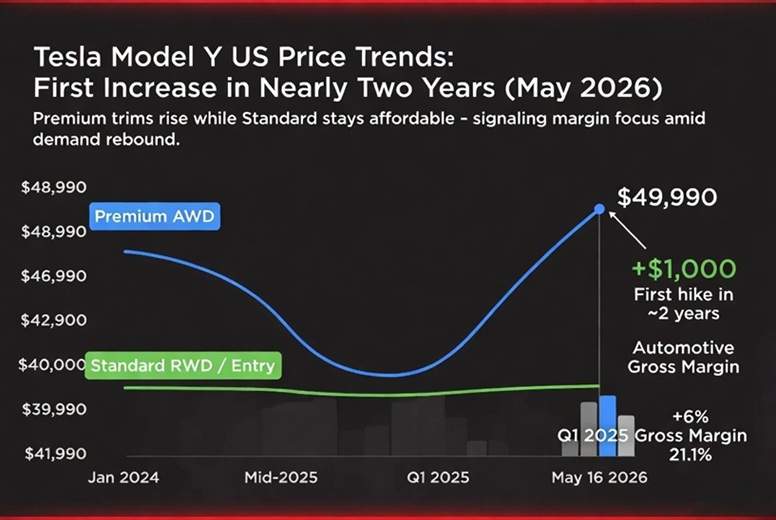

On or around May 16, 2026, Tesla made a move that caught many observers off guard: it raised prices on select Model Y variants for the first time in nearly two years. The Premium Rear-Wheel Drive climbed $1,000 to $45,990, the Premium All-Wheel Drive rose the same amount to $49,990, and the Performance version increased $500 to $57,990. Critically, the more affordable Standard (entry-level) trims stayed untouched.

This wasn’t a broad, across-the-board adjustment. It was surgical. And in the context of Tesla’s Q1 2026 results and its accelerating shift toward autonomy, the move reveals more about strategy than simple cost recovery.

Tesla has deliberately split the Model Y lineup. The Standard variants prioritize affordability with cost-optimized features: simpler interior trim, no panoramic glass roof in some configurations, smaller or fewer displays, and in certain markets, LFP battery chemistry. These keep the entry point competitive (starting around $39,990–$41,990 before destination) and support volume in price-sensitive segments.

The Premium and Performance trims, by contrast, deliver the fuller experience most buyers expect from a modern Tesla: ventilated and heated seats, ambient lighting, premium audio, full-width LED light bars, better ride quality via frequency-dependent dampers, panoramic glass, and longer range in many cases. These are the vehicles where feature differentiation—and likely higher gross margins—lives.

By lifting prices only on the richer trims, Tesla is doing something it has rarely done publicly in recent years: exercising selective pricing power on the higher-value end of the portfolio while protecting the affordable gateway that drives overall volume and brand accessibility. It’s a classic margin-volume balancing act, executed quietly.

Reading the Q1 Tea Leaves

Tesla’s Q1 2026 shareholder update painted a picture of stabilizing demand after a challenging period. Deliveries reached 358,023 vehicles, up 6% year-over-year, with a clear rebound in North America and Europe alongside continued growth in Asia-Pacific and South America. Inventory sat at a healthy 27 days of supply. Gross margins improved to 21.1%, and free cash flow came in at $1.4 billion with cash and short-term investments at $44.7 billion.

Record net new Full Self-Driving (Supervised) subscriptions and the shift toward a subscription-only model for FSD further signal that software attachment is becoming a meaningful profit lever—especially on higher-trim vehicles where buyers are more likely to opt in.

Raising prices on Premium and Performance variants right after this data drop makes strategic sense. It tests willingness to pay on the vehicles most likely to carry higher software and service revenue, without risking the volume momentum the cheaper Standard trims are helping build. In an environment where broader automotive prices have been rising across the industry, Tesla is simply reclaiming some of the ground it gave up during the intense discounting phase of 2024–2025.

The timing also aligns with Tesla’s longer-term product transition. In the same Q1 update, the company stated plainly that the Cybercab “will begin to replace the existing Model Y fleet and will be the largest volume vehicle in the fleet over time.” Pilot production of the purpose-built Robotaxi is already underway at Giga Texas, with volume production targeted for 2026 on an S-curve ramp.

As Cybercab scales for unsupervised Robotaxi duty, the personal-use Model Y naturally evolves. The higher-trim versions become the natural home for buyers who want premium features, longer range, and stronger FSD capability for personal ownership. Raising prices here now builds margin buffer exactly when Tesla is pouring capital into AI compute (Cortex ramps), battery vertical integration (Texas 4680 and cathode lines, Nevada LFP), Optimus factory preparation, and new Megapack capacity.

In other words, the price adjustment isn’t a reaction to weakness. It’s preparation. The cash generated from stronger margins on Premium Model Ys helps fund the very technologies that will eventually handle high-volume transportation through the Robotaxi network.

What This Means for Buyers and the Market

For customers, the message is clear: if you want the full Tesla experience—panoramic roof, premium audio, ventilated seats, and the latest hardware for FSD—the cost just ticked up modestly. The base Standard models remain the gateway for those prioritizing lowest entry price and efficiency (often with LFP chemistry advantages).

Competitors watching this move will note that Tesla still holds significant pricing discipline on its volume leader while demonstrating it can extract more where differentiation exists. With in-house battery production ramping (including dry electrode processes in Austin), Tesla’s structural cost position should continue improving, giving it flexibility on both the low and high ends of the lineup.

This small but symbolic price increase is best understood as part of Tesla’s multi-year pivot. The automotive business is stabilizing with better mix and software momentum. At the same time, the company is aggressively building the infrastructure for autonomy, robotics, and energy storage. Selective pricing power on the Model Y Premium trims is one quiet tool in that transition—generating incremental margin today while the Cybercab, Optimus, and next-generation AI compute scale for tomorrow.

It’s not flashy. It won’t generate the same headlines as a new vehicle unveil. But it’s the kind of disciplined, data-informed adjustment that separates companies managing through cycles from those simply reacting to them. Tesla just reminded the market that even its most mature product still has room to optimize for both volume and value—exactly the balance it will need as the Robotaxi era begins in earnest later this year.

Related Post

{kind=link}