Tesla (TSLA) will report Q4 2025 and full‑year 2025 financials on Wednesday, Jan. 28, after the market closes, followed by a management Q&A. Despite the “AI and robotics” narrative, the automotive business still drives the vast majority of Tesla’s results. With deliveries down for a second straight year but energy storage hitting records, here’s what Wall Street and retail investors are bracing for—and what to listen for on the call.

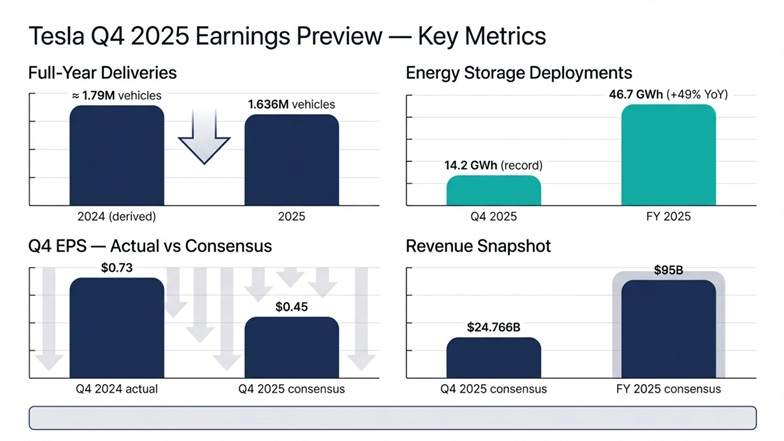

Q4 2025 deliveries fell 16% year‑over‑year versus Q4 2024 (company disclosed). 1.636 million vehicles, down 8.6% from 2024. Two years of declines. Energy storage: Q4 2025: Record 14.2 GWh deployed. 46.7 GWh deployed (+49% YoY). This is Tesla’s most consistent growth engine right now.

- Q4 2025 revenue: $24.766 billion (implies another YoY decline despite energy strength).

- Full‑year 2025 revenue: ~ $95 billion (about 3% below 2024).

- Q4 2025 EPS: $0.45 (down ~40% from $0.73 in Q4 2024).

- Full‑year 2025 EPS: ~$1.63 (down ~33% vs. 2024).

| Metric | Q4 2025 | YoY change | FY 2025 | YoY change |

|---|---|---|---|---|

| Vehicle deliveries | (Company: down 16%) | -16% | 1.636M | -8.6% |

| Energy storage deployed | 14.2 GWh | Record | 46.7 GWh | +49% |

| Revenue (consensus) | $24.77B | Lower YoY | $95B | ~-3% |

| EPS (consensus) | $0.45 | ~-40% | $1.63 | ~-33% |

What to listen for on the call (the real tells)

- Automotive gross margin (ex‑credits)

- How much did price cuts and incentive roll‑offs sting?

- Mix shift (Model Y vs. other) and any inventory cleanups.

- Energy storage margins and backlog

- Megapack demand, pricing discipline, and manufacturing cadence.

- Storage is scaling—are margins holding up as volume explodes?

- 2026 volume/production guide

- After two down years, does Tesla guide for growth—and how?

- Any factory capacity updates (Austin, Berlin) or new lines coming.

- New vehicle roadmap

- Concrete timing for lower‑priced models or fresh variants that expand the addressable market.

- If the answer is only “Cybercab” and Roadster teases, that’s a red flag for near‑term auto growth.

- FSD and Robotaxi reality check

- Safety metrics, regulatory progress, and cities/scale for pilot programs.

- Unsupervised timelines have slipped for years. What’s truly new?

- Optimus (humanoid robot) proof points

- How many units are deployed in Tesla factories, and what tasks are they performing?

- Hard numbers > glossy sizzle.

- U.S. incentives and pricing strategy

- Impact from lost credits or changing subsidy structures.

- Plan to stabilize average selling prices (ASPs) without sacrificing share.

- China/Europe competitive pressure

- How Tesla is responding to new EVs at sharp prices, especially from China.

- BYD passed Tesla in global EV sales—what’s the counter?

Top retail shareholder questions

SpaceX IPO allocation for long‑term TSLA holders, It’s telling that the top‑voted question is about another company. Expect no firm promises here. “When is FSD 100% unsupervised?” This question (and the answer “by end of year/next year”) has repeated for years. Investors need measurable, audited safety milestones. Robotaxi bottlenecks, Safety and liability are the core blockers. Any credible path must outline risk mitigation, not just software progress.

Optimus in factories—how many and doing what?

A factual count and defined tasks would be a meaningful update. Previous targets (5,000–10,000 units by 2025) haven’t materialized. New models for new segments (real cars customers can buy), The market wants fresh metal at more price points. Vague “soon” won’t rebuild confidence.

Tesla’s earnings and deliveries have declined while the global EV market keeps growing. The company also ceded the global EV crown to BYD in 2025. Storage is scaling fast and could become a more material profit pillar, but for now it can’t fully offset auto’s margin pressure. Since 2016, autonomy timelines have slipped again and again. Investors will reward tangible progress and near‑term product clarity over distant promises.

Stronger‑than‑feared automotive margin (cost take‑outs, mix), A clear 2026 launch for a lower‑priced vehicle, Storage margins holding firm with a bigger Megapack backlog, Concrete milestones for FSD safety/regulatory approvals in named markets. Another year of fuzzy guidance and “trust us, robotaxis soon”, No new consumer vehicle timelines, Energy margin compression as scale rises, Continued price whiplash that confuses buyers and hurts ASPs.

Going into Jan. 28, expectations are muted: lower revenue and EPS, shrinking auto margins, and a second straight down year in deliveries. The energy business is genuinely impressive, but it isn’t yet large enough to carry the whole show. If you believe unsupervised robotaxis and factory humanoids are imminent, the near‑term softness may look like a blip. If you need proof today, you’ll be listening for concrete 2026 volume guidance, a real new‑model roadmap, and steady storage margins. Talk is cheap; numbers and timelines are what matter now.

Related Post

{kind=link}