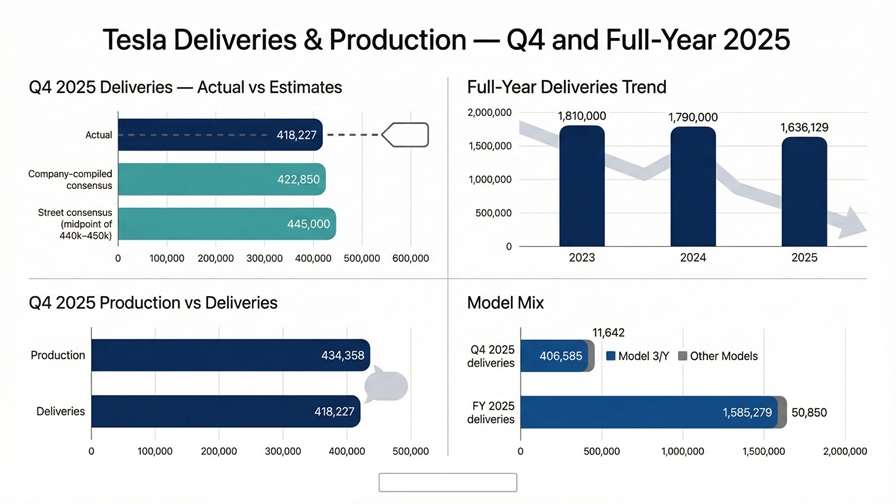

Tesla (TSLA) has posted its Q4 2025 and full‑year 2025 delivery and production results, and the headline writes itself: a second consecutive year of declines in EV deliveries — and the drop is getting steeper.

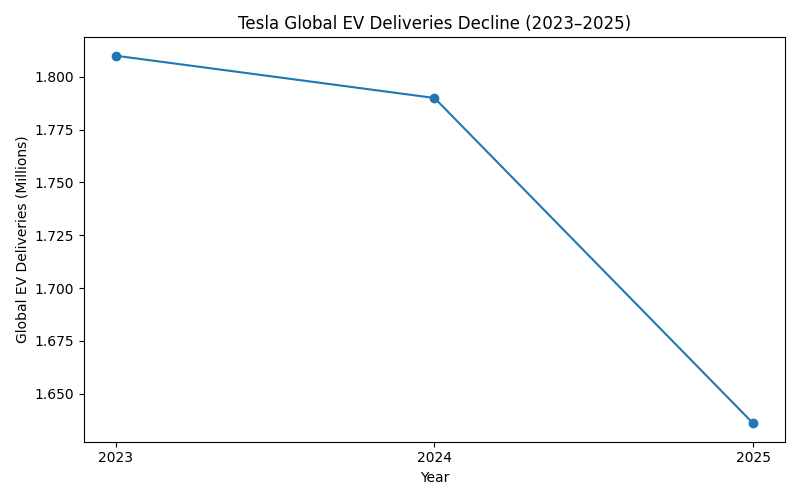

After peaking at 1.81 million deliveries in 2023, Tesla slipped to 1.79 million in 2024 amid an aging lineup and tougher competition, particularly in Europe. 2025 proved rougher still as brand headwinds, incentive shifts, and fiercer rivals in Europe and China piled on.

Q4 2025 scorecard

| Segment | Production | Deliveries | Notes |

|---|---|---|---|

| Model 3/Y | 422,652 | 406,585 | ~3% of deliveries subject to operating lease accounting |

| Other Models | 11,706 | 11,642 | ~5% of deliveries subject to operating lease accounting |

| Total | 434,358 | 418,227 | Deliveries down ~15% vs. Q4 last year |

Tesla did something unusual ahead of the print: it publicly shared a company‑compiled “consensus” of 422,850 deliveries based on 20 analysts — notably below broader public estimates in the 440k–450k range. The actual number (418,227) landed below both, signaling a softer close to the year.

Why deliveries are slipping

- Model lineup age: With limited all‑new nameplates in showrooms, price cuts and incentives have been doing the heavy lifting — and they only go so far.

- Competitive heat: Europe and China saw more credible EV alternatives at sharp prices, squeezing Tesla’s share and forcing tougher deal-making.

- Incentive changes: Shifts in U.S. incentives and regional policies affect take‑rates and timing, pulling some demand forward and pushing some out.

- Brand turbulence: Widely reported reputation issues can weigh on retail and fleet decisions, especially when buyers have strong alternatives.

Energy storage chalked up a record 14.2 GWh deployed in 2025. That’s meaningful for Tesla’s long‑term energy business — think grid‑scale batteries and commercial storage — and it diversifies revenue beyond cars. Still, the math is straightforward: automotive volume and margins remain the primary profit engine, and both were pressured by lower deliveries and a more promotional stance.

The growth era pause From 2013 through 2023, Tesla’s delivery climb was relentless. The last two years break that streak, underscoring how maturing EV markets and rising competition reshape the curve for even the category leader. It’s not the market — it’s the mix: Global EV adoption keeps rising, but growth is uneven by region and price band. With more brands in the game, share is harder to hold without fresh metal.

If you’re EV‑curious, the market is more negotiable than it was a year ago. Watch for end‑of‑quarter promos, inventory deals, and financing offers — from Tesla and its rivals. Lower deliveries don’t change your day‑to‑day, but service capacity and software updates remain the things to watch. Tesla tends to keep OTA updates flowing. Two straight annual declines in deliveries usually translate to pressure on revenue and earnings unless offset elsewhere. Storage helps, as do software and services, but vehicle mix and pricing will drive the P&L near term.

Elon Musk has been framing Tesla’s future around AI — Full Self‑Driving, robotaxi, Optimus — as the next growth leg. If you buy that thesis, near‑term delivery dips may feel like noise. If you want line‑of‑sight to profits today, you’ll be looking for tangible progress on:

- FSD take‑rates and safety/performance milestones

- Regulatory approvals for supervised or driverless operations

- Clear commercialization timelines (fleet scale, revenue per mile)

- Hardware readiness (camera/sensor suites, compute, maintenance)

Any significant Model Y/3 updates, or a new mass‑market model, could reset the demand curve. Fewer mid‑month price swings and clearer trim walk‑ups would help buyers commit. Europe and China will continue to be the bellwethers for whether pricing or product does the talking. Can Tesla compound that 14.2 GWh in 2026 while improving margins? Production vs. deliveries gap is a tell for inventory discipline and demand pacing.

Tesla closed 2025 with 418,227 deliveries in Q4 and 1,636,129 for the year — down 15% year over year in the quarter and 9% for the full year. That’s two straight annual declines after a decade of near‑constant growth. The energy business is hitting records, but the core automotive story needs fresh product, steadier pricing, and cleaner regional execution to reignite momentum.

If you’re all‑in on Tesla’s AI and robotaxi vision, the near‑term dip may look like a pit stop. If you’re focused on the current scoreboard, 2026 will be about proof: new models, better mix, and consistent delivery beats — not just big promises.

Related Post

{kind=link}